Looking Beyond The Google & Wiz Acquisition: The Future Of Cloud Security

The consequences of the acquisition between Wiz and Google and how it changes the future of the cloud security landscape

By this time, you’ve likely read extensively about the acquisition news earlier this week. My goal is to aggregate some of the best resources and provide a nuanced, differentiated perspective as someone who has spent significant time with some of the co-founders, many Wiz team members and many of the leading cloud security vendors over the past few months. This piece focuses on the evolution of cloud security due to the acquisition and its impact on competitors + frenemies.

Key Summary

Goals of this report: Last year, I wrote extensively about Wiz in this deep-dive report and co-published a report with James Berthoty, on the broad state of cloud security here. Since many readers broadly know the pros and cons of this acquisition, I have shaped this report as an aggregation of the best ideas, my contrarian takes, and a focused discussion on the future of cloud security. It also aims to educate readers who might be unfamiliar with either Google Cloud’s ambitions or why Wiz was such a highly valued company. This piece is written in a format that’s easy to skim through over within a few minutes.

A once-in-a-generation technology company: Wiz was on the verge of becoming the second-ever company after OpenAI to achieve $1B in revenue within five years (2020-2025). No prior technology company had accomplished this feat, let alone a cybersecurity company. This was due to a near-flawless go-to-market execution and its agentless, graph-based security model. It was unique among the Fortune 100—turning cloud security into a boardroom priority post-2020, even though cloud security had existed for over a decade. Wiz arrived with the right product, the right GTM, and the right team—at exactly the right moment.

Competitive wars in cloud security: This deal intensifies competition among major vendors like Palo Alto Networks, CrowdStrike, and smaller cloud security startups. While Wiz has gained Google’s resources, there is a risk that hyperscaler ownership may push some multi-cloud enterprises to seek independent security solutions. Competitors and niche startups could capitalize on any customer hesitation about Google lock-in. Runtime security is the future of cloud security. I had been working on a major report covering Wiz’ CDR next month (which will still be launched)

Cloud & AI security: It is important not to lose sight of the bigger picture. Google is going head-to-head with OpenAI in the AI race. Every dollar spent on cybersecurity—and subsequently, AI models deployed in the cloud—should drive greater consumption of cloud services. Google wants that cloud spend on GCP, not on Azure or AWS. As AI initiatives (e.g., Gemini, Azure OpenAI) continue to reshape the industry, the synergy between robust security and rapid cloud adoption will become even more pivotal.

Integration Challenges & Vendor Neutrality Concerns: Maintaining Wiz’s brand independence, culture, and multi-cloud support will be critical. If Wiz is perceived as “Google-first,” large enterprises running workloads on AWS or Azure may switch to neutral security providers. Ensuring Wiz retains its speed, innovation, and trust will be essential for Google to realize the full value of the acquisition.

Historic deal - Financial Metrics

We already know this is the largest-ever acquisition by Google. Wiz’s acquisition price is higher than the combined total of Alphabet’s eight other largest acquisitions (which included Motorola Mobility at $9.6B and Mandiant at $5.3B). Those eight largest acquisitions totaled $29 billion; Wiz alone is $32 billion.

Alphabet reportedly offered $23 billion for Wiz in July 2024. The eventual $32 billion price is about 39.1% higher than the earlier figure. This shows Google’s desperation as it realized it was losing market share as the third public cloud player relative to other players. This deal signals Google’s increased commitment to cybersecurity, potentially accelerating further M&A. Wiz’s exit removes a fast-growing independent competitor from the market, impacting rivals like Palo Alto Networks, CrowdStrike, AWS, and Microsoft in different ways.

Why Wiz Was (Likely) Worth $32B?

I wrote an extensive analysis based on discussions with Wiz’s original founders, team members, and customers. Please read the full report here. I’ll summarize the key takeaways in five points:

1/ Remarkable execution

To understand why a company paid such a premium multiple for Wiz, we need to start by understanding whether the financial metrics make sense. Wiz was the fastest-growing company to reach $100M ARR, then $300M, and subsequently $500M. According to rumored metrics, as of the beginning of this year, Wiz was around $700M ARR. Based on my contacts close to the deal, they were on track to surpass $1.1B by the end of this year. At this point, if you didn’t have Wiz, a CISO could be questioned.

2/ Dominance within cloud security

Wiz’s rapid dominance in the cloud security space is reflected in its revenues. Only CrowdStrike comes close right now.

Commentary on the stated figures:

Wiz is estimated to be around $700M–$800M (based on my sources)

Prisma Cloud last reported metrics as of last year (2024)

CrowdStrike reported its metrics in its recent quarter (Q2 2025)

SentinelOne has never given its full breakdown, as well as the rest, so take these with a grain of salt (however, I have my sources that confirm many of these numbers are accurate).

For context, when Prisma Cloud had around $100M in early 2020/2021 (together with the AppSec acquisitions it tucked in), Wiz was at a single-digit revenue. Over the years, their rapid growth allowed them to close the gap with Prisma Cloud. The last time Palo Alto Networks reported Prisma Cloud revenues, it was around $700M, and growth had slowed down. However, some external metrics showed how fast Wiz was growing.

Wiz’s growth has been nothing short of impressive. Based on my sources, Wiz feasted on the losses of Lacework. This is particularly impressive given that Wiz, founded in 2020, reached this scale in just a few years, far outpacing competitors who have been in the industry for a decade or more. In comparison, companies like SentinelOne ($150M), Orca ($110M), Lacework/Fortinet ($100M), and Sysdig ($100M) are still far behind in revenue scale.

This revenue disparity underscores two key takeaways:

Wiz not only built a best-in-class security product but also executed a near-flawless GTM strategy, allowing it to outpace the competition.

The company’s relentless customer focus, frictionless onboarding, and deep integration with cloud providers contributed to one of the fastest revenue growth trajectories in cybersecurity history.

3/ Why Wiz dominated cloud security

I’ve detailed everything extensively in this old report. However, in a few words. Wiz nailed the cloud buyer experience (ease of use, quick deployment) and architectural design (graph, agentless) of the product. I’ll break it down:

*Truly* customer-obsessed culture: I heard some crazy stories from the founders themselves and even their customers about the depth of customer focus at Wiz, which was remarkable. Numerous stories highlighted how deeply the team cared about customer needs and continuously improved the product.

Product excellence through architecture (Backend): Wiz revolutionized cloud security with two key innovations: a graph database approach that connects security risks across cloud resources, and agentless scanning for rapid deployment. The graph database enabled contextual analysis of security risks, eliminating isolated asset scanning and reducing false positives. This allowed organizations to better prioritize threats and identify dangerous vulnerability combinations.

Foundation in agentless architecture: Wiz pioneered the graph database approach to cloud security misconfiguration (further enhancing earlier innovations from Orca's agentless scanning). This approach allowed them to connect risks across multiple cloud resources with contextual insights—a capability their predecessors struggled to deliver effectively. From a technical standpoint, Wiz's strength lies in rapid agentless vulnerability scanning, asset management, and the ability to scan snapshots and manage cloud assets across multiple platforms.

Seamless user experience (Frontend): The product's ease of deployment and immediate value delivery resonated with time-constrained security teams, enabling rapid adoption without complex sales cycles. It was agentless and quick to deploy, providing immediate visibility across risks. This is a rare enterprise product that promised to deliver impact from Day 1. That’s not luck—it’s intentional design. Founders, find a critical, underserved pain point, and deliver value lightning-quick. Ultimately, Wiz achieved frictionless product-led growth through seamless onboarding, making it an obvious choice for users.

4/ Best-In-Class Go-To-Market (GTM) Execution, Brand Building & Enterprise Focus

Wiz had an enterprise-first GTM strategy, targeting Fortune 500 companies from day one and leveraging its Microsoft experience to build for scale. It strategically leveraged cloud marketplaces (AWS and Azure), reducing sales friction and making it easy for enterprises to purchase and deploy. The co-selling model with hyperscalers (AWS, Microsoft), helped Wiz penetrate large accounts efficiently.

Similarly, in its early days, Wiz sold directly to CISOs—high stakes, high-touch, and high ACVs—the kind of enterprise motion everyone assumes takes years. Wiz broke that rule. No freemium. No self-serve. Instead of rapidly hiring a large sales force, Wiz focused on recruiting elite, high-performing sales reps in the early days, many of whom consistently hit 1000% of quota. Many sellers came from competitors and many came from unusual backgrounds. The success of Wiz wasn’t just about having a good product. It was about a well-executed go-to-market strategy that involved understanding the needs of the customer, creating virality, and dominating the narrative. This approach is presented as a model for success in the cybersecurity industry. They successfully penetrated 50% of Fortune 100! This is another amazing post that discusses all the factors to Wiz GTM success, a playbook for any GTM team.

5/ Perfect Market timing & Capitalizing on major cybersecurity incidents:

Wiz launched in 2020, just as enterprises were accelerating cloud adoption due to the pandemic, creating a massive demand for scalable, cloud-native security solutions. The Log4Shell vulnerability crisis (2021) was a pivotal moment since Wiz’s graph-based model allowed customers to quickly identify and remediate impacted cloud assets, driving a surge in enterprise adoption. Unlike earlier cloud security vendors that focused on isolated misconfigurations, Wiz provided contextual, actionable insights when enterprises needed them.

6/ Ambitious leadership & talent density

Wiz’s founding team—Assaf Rappaport, Yinon Costica, Ami Luttwak, and Roy Reznik—had deep cybersecurity expertise, having previously built and sold Adallom to Microsoft. The founders had worked together for over two decades, fostering trust, rapid decision-making, and seamless execution. They built a high-intensity culture that attracted top-tier talent from Microsoft and the Israeli military (Unit 8200/Talpiot).

Wiz’s remarkable GTM execution was driven by a combination of user-centric design, seamless adoption, community-driven momentum. Wiz out-executed competitors through product innovation, GTM excellence, a high-caliber founding team, and aggressive expansion. By solving a real enterprise pain point with a novel approach (graph-based security) and riding perfect market timing, Wiz became the fastest-growing cybersecurity company in history.

Why Google Made The Acquisition

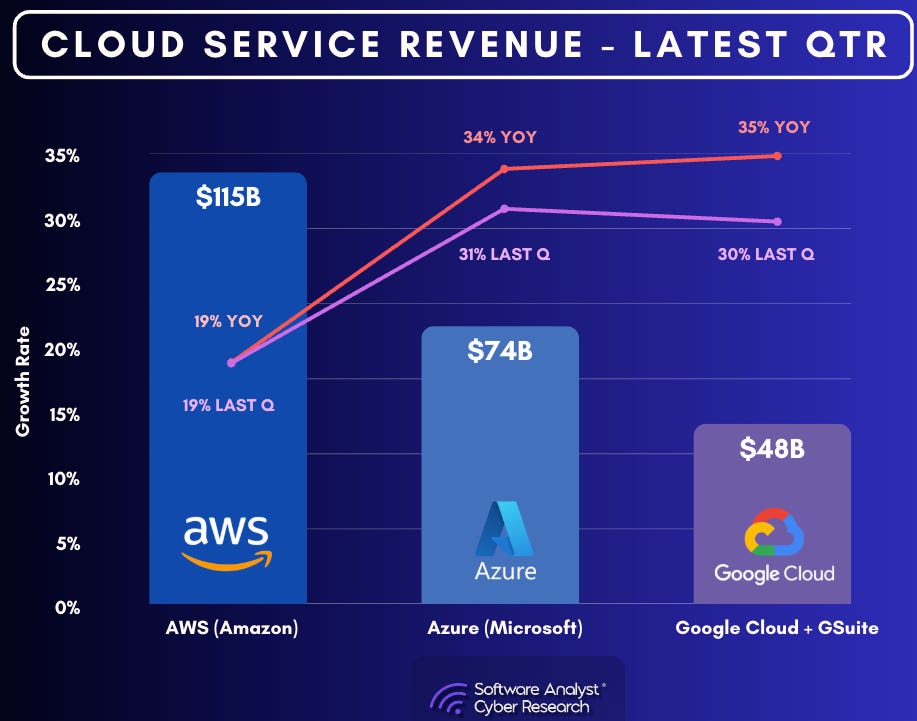

1/ Google was losing cloud market share

Google had the weakest growth rates among major hyperscalers.

Their overall ARR growth had slowed down, and they needed something big to revive momentum. This led to their investment in Wiz—a strategic move to gain access to cloud security.

If we analyze the run rate growth rates from the most recent quarter, we’ll see that Google Cloud’s growth slowed down. While not a dramatic decline, it was clear that Google wasn’t catching up as fast as its competitors.

2/ Google Was Losing In Cybersecurity

Although Google has been investing in security, it remained (far) behind Microsoft and AWS in terms of enterprise adoption. The $5.4B acquisition of Mandiant expanded Google’s incident response and threat intelligence business, but Google still lacked a strong foothold in anything security, where AWS and Microsoft had established offerings.

Microsoft: Microsoft Defender for Cloud was already a big business. However, it’s important to note that Microsoft’s biggest strengths in cybersecurity have primarily been in Identity, Security Operations, and Endpoint Security.

AWS: AWS has a broad range of capabilities in cloud security but has primarily been strong in infrastructure protection.

Wiz gives Google an agentless cloud security platform with a huge data advantage, built on Wiz’s graph. I can’t emphasize enough how fine-tuned and rich the data Wiz has from its graph, which provides enriched contextual risk analysis and broad multi-cloud visibility—areas where GCP’s existing security stack has been weaker. This acquisition helps Google Cloud Security become a more serious contender in cybersecurity, but it also raises questions about how Google plans to integrate and scale Wiz within its ecosystem.

How Does Wiz Solve It?

1/ Furthering Google’s AI + Cloud Ambitions

A big growth vertical that isn’t discussed enough is how modern AI models are rapidly deployed on the cloud. With applications being built faster using tools like GitHub Copilot and Cursor, we can anticipate significant acceleration in both cloud applications and AI workloads deployment. As a result, cloud adoption continues to grow, while AI-driven workloads introduce new security risks that existing tools are still adapting to.

Google has big ambitions around AI and is positioning itself to compete with OpenAI and Microsoft across Search, Gemini, and broader LLM applications. To establish itself as a leader in AI, Google must secure AI models, training data, and inference pipelines in the cloud—a major opportunity for growth in security.

Wiz had already been investing in AI Research and AI Security Posture Management (AI-SPM)—a growing area as companies realize AI systems introduce new security risks around data governance, model tampering, and unauthorized API access.

Wiz already has strong visibility into cloud infrastructure, which extends into securing AI workloads. However, AI also increases the complexity of securing cloud environments, and many enterprises lack visibility into their AI-driven infrastructure. The combination of Wiz’s graph-based approach and Google’s AI security research (Chronicle, VirusTotal AI, Sec-PaLM) could help differentiate Google’s security portfolio. However, integrating these capabilities into a cohesive AI cloud security strategy will be a major challenge but a necessary direction.

Google’s investment in AI security (Sec-PaLM, Gemini, AI Red Teaming, and AI model monitoring) aligns well with Wiz’s AI-SPM strategy.

A combined platform could provide customers with:

Visibility into AI model infrastructure running in the cloud.

AI-driven threat detection, combining Wiz’s graph-based risk analysis with Google’s AI security research.

Stronger security posture management for AI workloads, addressing data security, API security, and model integrity.

If executed well, this could become one of the first truly cloud-native AI security platforms. However, its success will depend on how seamlessly Wiz’s AI security features integrate into Google’s broader AI security strategy.

Google has positioned itself as a leader in AI, but securing AI models and workloads in the cloud remains an unsolved challenge. AI models are increasingly hosted and deployed in cloud environments, making cloud infrastructure security a foundational requirement for AI security.

2/ Filling Gaps in Google Cloud’s Security Offerings

This area has been discussed extensively, but Wiz strengthens several weak points in Google Cloud’s security portfolio.

Let’s begin by reviewing GCP’s existing security offerings:

Security Operations Center (SOC): Google’s Chronicle SIEM and XDR provide strong log analysis. This has arguably been Google’s best-performing security product. Wiz brings better cloud security data to enhance threat detection, correlation, and response. However, there will be friction points—they will need to incorporate vulnerability data to help SOC teams manage large data volumes effectively.

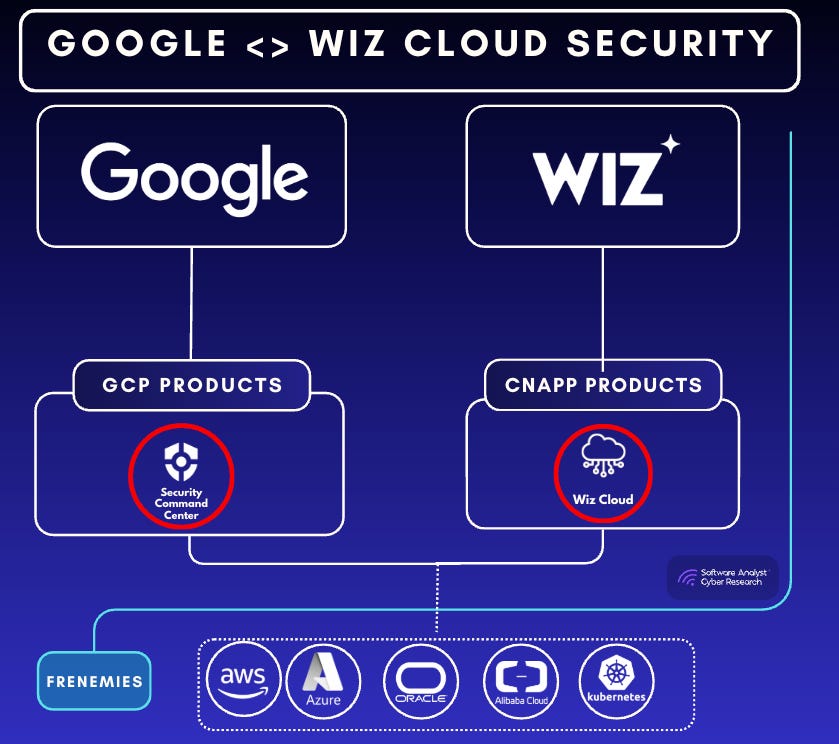

Google Security Command Centre: This is Google’s most relevant security product. Wiz enhances Google’s ability to detect misconfigurations, assess risk, and provide multi-cloud security insights. Integrating Wiz into the Security Command Centre (SCC) could make Google’s cloud security platform more competitive, but it also risks making Wiz feel like a Google-first tool rather than a truly independent multi-cloud solution.

Mandiant Consulting Services Incident Response: Mandiant provides forensic and response capabilities. Moving forward, this will likely give Google stronger remediation capabilities, enhancing its cloud security foundation for preemptive defense.

Threat Intelligence: Google unveiled its Threat Intelligence offering at RSA Conference 2024, integrating capabilities from Mandiant, VirusTotal, and Google's own security data (The service leverages insights from over 1.5 billion Gmail accounts, 4 billion devices, and Mandiant's extensive incident response experience)

Google has been striving to build a cohesive cloud security and TIDR (Threat Intelligence, Detection, and Response) framework—often referred to internally as a single “security fabric.” By integrating Wiz’s CNAPP platform and security graph, Google aims to make cloud security a primary focus within its broader security ecosystem. This includes leveraging Chronicle for log analysis, Mandiant for incident response, and VirusTotal for threat intelligence. The goal is to bundle and unify these capabilities into a single, comprehensive offering that simplifies cloud security management for enterprise customers and strengthens Google’s position in the multi-cloud security landscape.

3/ Wiz Strengths Google’s Position in Multi-Cloud Security - against AWS, but probably Microsoft

Google Cloud has struggled to compete with AWS and Microsoft in enterprise adoption, largely because many large companies already have deep investments in those platforms. Microsoft has strong security products in identity and endpoint protection, but its cloud security tools lag behind its broader security suite. AWS, meanwhile, offers many security features, but its cloud security solutions are fragmented and often require third-party tools.

Wiz gives Google a compelling security platform that protects AWS, Azure, and Google Cloud workloads, allowing Google to sell into organizations that aren’t fully committed to its cloud services. This is a strategic move to position Google Cloud as a serious player in multi-cloud security. However, the challenge is that customers may hesitate to trust a hyperscaler-owned security tool monitoring their AWS and Azure environments.

4/ Leverage & build Insights upon Wiz’ Cloud Vulnerability DB

As an independent company, Wiz’s graph-based scanning CNAPP was its secret weapon, enabling deep multi-cloud insights. With this acquisition, Google will further enhance the Wiz Graph with additional context and intelligence, making it even more effective in identifying vulnerabilities across multi-cloud environments.

5/ Wiz Now allows Google to access more Fortune 100 Enterprises

Wiz had a strong foothold in the Fortune 100, with over 50% adoption among large enterprises. Google Cloud struggled with enterprise adoption compared to AWS and Microsoft (AI tailwinds fueled AWS and Microsoft’s growth, leaving Google behind). Google realized they needed a growth catalyst. Wiz provided the perfect entry point to sell security and cloud services to large enterprises. However, the question remains: Will enterprises want to buy security from Google? Many security leaders prefer independent vendors over hyperscaler-owned solutions. If Wiz becomes too integrated into Google Cloud, customers may shift to alternative multi-cloud security providers like Crowdstrike, Palo Alto Networks, Orca, Sysdig etc.

6/ Acquiring a highly talented team

Wiz’s founders, engineers and brand marketing teams are some of the most talented people, not just in cybersecurity but all of technology. The founders bring deep expertise, building on their experience from Adallom and their years spent in cybersecurity leadership.

Retaining this team is critical for Google to extract value from the acquisition, as cybersecurity expertise is difficult to scale within large organizations. However, Google’s culture and structure are vastly different from Wiz’s fast-moving, independent approach, and there is always a risk that key leaders and engineers may leave after the integration period.

Implications for Cloud Security Competitors

Impacts on the broader ecosystem

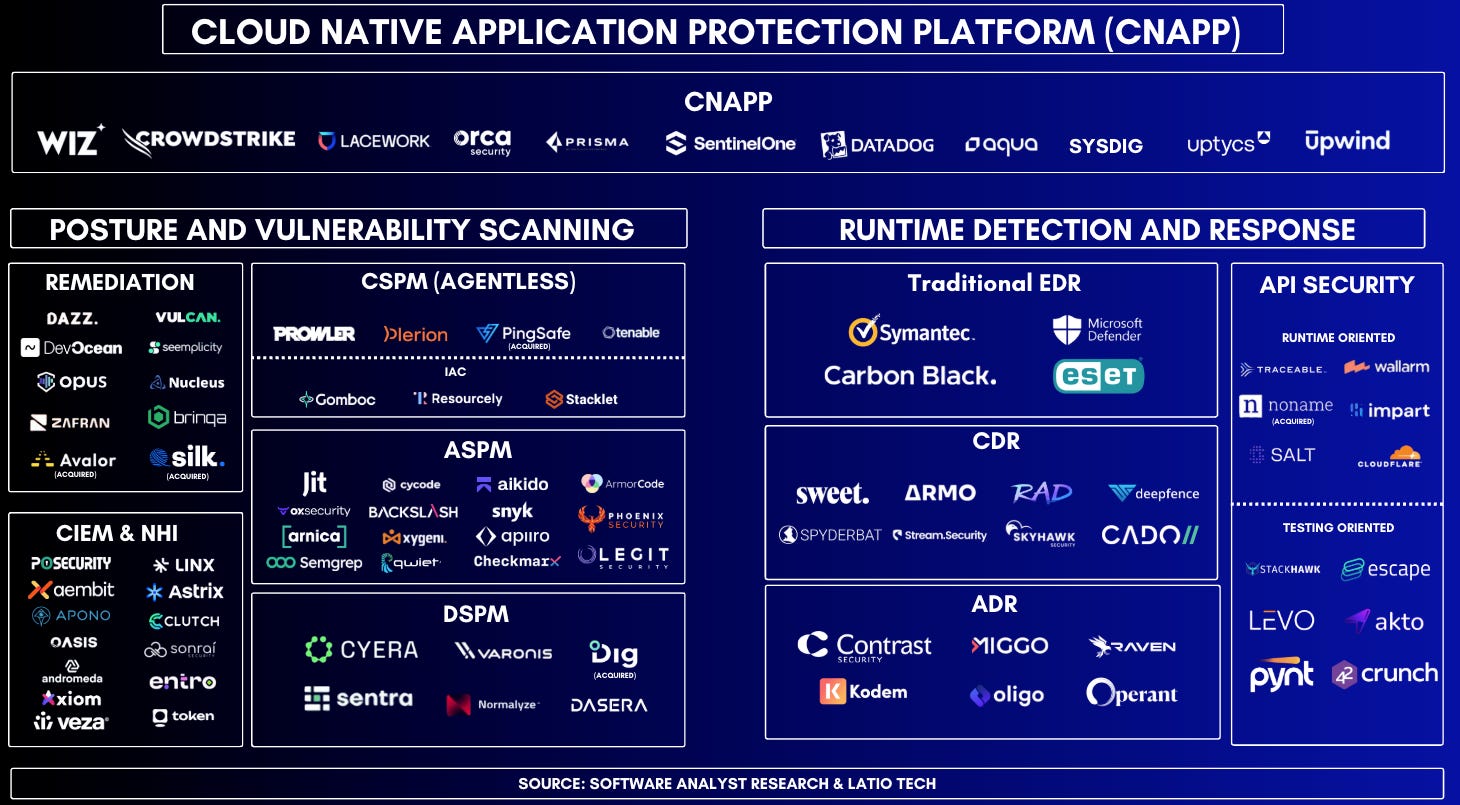

Last year, together with James Berthoty - I put together a broad cloud security ecosystem report. The whole cloud security market and its adjacencies can be seen below.

This acquisition has far-reaching implications for cloud security, more so than other categories of cybersecurity. Many haven’t discussed it extensively, but I believe this shines a spotlight on both established players like Palo Alto Networks (PANW), SentinelOne, and Sysdig, as well as emerging startups such as Upwind, Sweet Security, and Armo. This could actually create a window of opportunity for these competitors to raise awareness of their offerings. However, gaining significant market share won’t be easy. Wiz now has Google’s resources and reach behind it, and that competitive edge will likely prove tough to match.

For established vendors, brand recognition and integrated solutions are clear advantages, but they face intensified pressure to differentiate and innovate against "Google + Wiz." Meanwhile, cloud-agnostic approaches like Cortex Cloud could benefit if friction arises between Google and Wiz, as organizations might favor independent solutions. Ultimately, this deal raises awareness of cloud security, but capturing significant market share will remain difficult in a landscape where securing agile, cloud-native environments becomes ever more critical.

Big winners likely will be multi-cloud competitors

Crowdstrike

If this acquisition goes wrong somehow, some of the biggest winners could likely be CrowdStrike and Palo Alto Networks. These two companies have been aggressively consolidating cloud security.

CrowdStrike has been experiencing significant momentum in its cloud security products. It was the closest competitor to Wiz, giving them a hard time before today. Also, remember that CrowdStrike had an advantage in performing better CSPM scanning capabilities in Windows environments. It was already expanding that capability across Linux and other environments with further bundling measures.

At around $100M–$200M ARR, CrowdStrike has been growing rapidly. If Wiz’s innovation and ambitions slow down, CrowdStrike will quickly catch up.

Palo Alto Networks

Palo Alto Networks (PANW) has been doubling down on cloud runtime security with its new Cortex Cloud. This product consolidates SIEM, XSIAM, and CNAPP functions into a single console, allowing different teams to work more effectively. It’s possible Google Cloud will take a similar approach after acquiring Wiz—perhaps paying a premium because of PANW’s moves, given that Google already had some similar SOC offerings.

Although growth for Prisma Cloud has slowed in recent quarters, PANW still reports a 50% increase in total bookings and a doubling of deals over $1 million. Compared to Wiz, PANW’s solution stands out for its stronger runtime security and endpoint protection—areas Wiz may rapidly improve with Google’s backing. Still, it remains to be seen if Wiz can truly close that gap.

Because Cortex Cloud is cloud-agnostic—much like CrowdStrike—PANW could benefit if any friction arises between Google and Wiz. If that happens, organizations might look to alternative providers that offer robust, independent cloud security.

Adjacent cloud competitors

Data security competitors: Competitors including Cyera, Laminar (Rubrik), and Varonis stand to benefit. Many have forgotten that Wiz had been a prominent name within data security posture management (DSPM) category, but with this acquisition, Google may de-prioritize certain aspects of its data security focus.

Application security: Wiz had been investing strongly into AppSec and Code. Competitors included companies like Veracode, Checkmarx, and Snyk. With this acquisition, it is likely that Wiz will shift focus away from this category.

AI-SPM competitors: Companies like Protect AI, HiddenLayer, and Palo Alto Networks had been developing robust AI workload scanning capabilities for securing AI in the cloud and stand to gain an edge “if“ the market shifts. However, if Google double downs into AI cloud workloads, it will significantly affects these players.

Overall, this acquisition will have far-reaching implications for the competitive ecosystem. There will be an increased need for companies to develop specialized, differentiated cloud security solutions that offer vendor independence. This move will likely drive Wiz to double down on its core cloud scanning product, while simultaneously opening opportunities for new startups to innovate in adjacent areas.

As Google and Microsoft expand their cloud security offerings, new startups may emerge with highly specialized tools to address gaps where larger players are still evolving. However, the actual implications for startups remain largely unknown.

In the short term, CISOs who prioritize vendor neutrality and certainty will likely turn to smaller, specialized startups in the cloud security and application security domains. These startups still have work to do as CISOs care about the best solution. These startups must now up their game and will need to differentiate themselves through unique feature sets or by focusing on emerging markets, such as runtime protection or AI-driven threat detection.

Potential Challenges: Analyzing Pros & Cons

Below is my raw analysis, questions, and considerations of the consequences of the acquisition.

1/ The challenge of integration without stifling Innovation: Google is an innovative company (compared to Cisco or traditional firewall companies)

There is also the hypothesis that Google isn’t a traditional company and will work closely to maximize value from Wiz rather than stifling its momentum.

Product Integration Risks: Wiz’s platform is built on AWS, not Google Cloud. Harmonizing architectures across different infrastructures could slow down innovation.

Google’s Track Record on Acquisitions: Many products acquired by Google have lost independent momentum post-acquisition. Wiz’s success was largely driven by its speed and agility, which might be difficult to maintain within Google’s corporate structure.

Balancing Independence vs. Integration: If Wiz becomes too integrated into Google’s security stack, it may lose the market trust and differentiation that made it successful in the first place.

2/ Vendor lock-In concerns, but why retaining Wiz’ “Brand“ is a non-negotiable

Wiz’s reputation is built on supporting AWS, Azure, and Google Cloud equally. If Wiz becomes simply “Google Cloud Security,” organizations may suspect lock-in or a GCP-first mentality. CISOs will worry about losing flexibility when their cloud security vendor is owned by a hyperscaler. Google’s ownership could make Wiz feel like a less neutral security partner since many enterprises have multi-cloud architectures to avoid overreliance on a single provider. If Google subtly integrates Wiz too deeply into Google Cloud’s ecosystem, customers may feel pressured to adopt more Google-native solutions leading to resistance IMO. Hence, I truly believe that retaining Wiz’s strong, independent brand is key to helping customers stay confident they can secure their workloads anywhere. Removing Wiz’s identity risks losing the goodwill that grew from its agile startup roots.

This uncertainty could slow Wiz’s momentum

CISOs may hesitate to adopt Wiz post-acquisition, fearing product changes, vendor lock-in, or strategic shifts that align Wiz more with Google Cloud than with multi-cloud environments. Enterprises using AWS and Azure may explore alternative CNAPP solutions (e.g., Palo Alto Prisma, Orca, CrowdStrike Falcon) instead of relying on a Google-owned security platform.

3/ Regulatory scrutiny could delay or block the deal

Although many believe this deal will go through under an M&A-friendly administration, I still believe regulatory scrutiny is inevitable given the size of the acquisition and its impact on competition. Competitors in this space will silently lobby against it, making it a potential target for antitrust challenges. Regulatory bodies may examine whether Google is gaining an unfair advantage in cloud security. The deal could be challenged on anti-competitive grounds, particularly if Google bundles Wiz with Google Cloud to disadvantage AWS and Azure customers. Regardless of the outcome, Wiz still wins in that Google could pay Wiz $3.2 billion, if acquisition falls through. The deal is set to face a lengthy regulatory review, which will be a significant win-win for Wiz regardless of the outcome.

4/ Risk of Wiz losing focus & letting go on new growth areas in cloud

We know that Wiz will continue to go aggressively on runtime cloud security because this is Google cloud’s DNA already. However, I believe Wiz’s ability to compete in Application Security Posture Management (ASPM) will have to take a backseat to emphasize other areas (or, we could see Google make more acquisitions here!). If it loses focus under Google, startups will move aggressively to fill the gaps. Alternatively, the security industry is shifting towards consolidated, full-stack security solutions. If Wiz remains too narrow in scope, i.e. only CSPM because of this deal and how Google may only use the core CSPM scanning graph, it may lose relevance in the evolving market.

5/ Market perception & potential trust issues

The key question: Google Cloud customers may benefit—but at what cost?

There are some data access & privacy fears, which I suspect are overblown. There is a tremendous advantage of data that could benefit Google cloud, but what are the costs? Will it even happen? (I doubt so, GCP wont be so silly - I hope). However, let’s explore the possibilities - the pros and cons.

There are huge trust & data segregation concerns. While Google will assure data segregation, its history with privacy controversies makes some customers skeptical about how Wiz’s multi-cloud telemetry will be used. Even if Google does not misuse data, AWS and Azure customers may worry that Google gains insights into their security practices, which could be used against them in future cloud deals.

The challenge will be maintaining Wiz’s neutrality. We know customers may fear that Google will prioritize its own cloud services at the expense of AWS and Azure integrations. Alternatively, we know Google could leverage Wiz’s security data to tailor pricing models or offer custom discounts to incentivize enterprises to shift workloads to Google cloud. This creates a competitive distortion, potentially leading to favoritism or pricing manipulation—a scenario that would not exist if Wiz had remained independent.

There is also the risk of conflicts of interest, where customers may question whether Google’s ownership will alter Wiz’s product direction to benefit Google Cloud at the expense of AWS and Azure customers. Historically, multi-cloud security vendors acquired by cloud providers have struggled to maintain neutrality. If Wiz is perceived as too Google-centric, multi-cloud customers may hesitate to continue using it.

How Most of These Issues Should Be Solved

Retaining a Founding Visionary: Keeping at least one of Wiz’s co-founders (e.g., Assaf or Yinon) on board ensures continuity of culture, vision, and innovation. A founder’s presence can energize the team, encourage top performers to stay, and help push ambitious product roadmaps that might otherwise stall under a large corporate umbrella.

Transparent Communication with Stakeholders: To maintain trust—especially for multi-cloud users—Google and Wiz must be upfront about their roadmap, data handling, and ongoing service commitments. If they don’t proactively address concerns around potential vendor lock-in or favored integration with Google Cloud, AWS and Microsoft are likely to sow doubt and lure away security buyers.

Meanwhile, CISOs have to watch the fine print. Thoroughly reviewing post-acquisition terms and agreements is critical for clarifying data governance, pricing changes, or any shifting SLAs that might affect compliance or vendor neutrality.

Future of Cloud Security:

Bundling Era

A Google “security bundle” built around Wiz could excel by unifying threat detection, posture management, and incident response into a single console—merging Wiz’s CSPM strengths with Google’s SOC capabilities (Chronicle, Mandiant, VirusTotal) for a holistic view of cloud risk. Tight integrations with Google Cloud services (IAM, Kubernetes, logging) would further streamline protection for cloud-native workloads, while still supporting multi-cloud environments. Adding developer-friendly features—like automated scans in CI/CD pipelines—would shift security left, catching issues early and reducing remediation costs. Offering these components under flexible, all-in-one licensing agreements could drive both adoption and cost savings for enterprises seeking a simpler approach. Yet, the flip side is potential vendor lock-in: as Wiz becomes more deeply intertwined with the GCP stack, organizations might lose some freedom to mix and match solutions across different clouds.

Stronger Runtime Security Capabilities

Google has historically been runtime-heavy, with deep investments in detecting, analyzing, and responding to real-time threats. Solutions like Chronicle SIEM, Mandiant Consulting & Incident Response (IR), and Google Security Operations.

Wiz, in contrast, brings lots of strengths in agentless cloud security, focusing on misconfiguration detection, toxic combinations, and attack path analysis. More recently, Wiz has expanded into runtime security with Wiz Defend and acquired Gem Security (for Cloud Detection & Response).

Bringing Google’s threat intelligence and runtime detection together with Wiz’s cloud security posture management (CSPM) and agentless visibility creates a stronger end-to-end security offering. Customers will get real-time attack detection, cloud misconfiguration alerts, and deep cloud workload protection—all within a unified platform. But, they will have to navigate the tensions and split between the different users across these segments of products.

Summary

The Wiz acquisition underscores the rising premium on cloud security as businesses migrate to multi-cloud and AI-driven architectures. Many traditional security tools struggle with cloud complexity, but regardless of where you stand in this scenario, Wiz has built something the market needs at precisely the right time. It has reignited interest in M&A and has inspired many more cybersecurity companies to think about the future. Ultimately, the battle for cloud security dominance is far from over, and the true impact of this acquisition is yet to unfold.

Best Resources / Additional Readings

Cole Grolmus’ consolidated analysis: Alphabet’s Audacious Acquisition

That’s an outstanding write up. Thanks for putting in the hard yards on this.

Great article; IMO, Console integration would be key to determining if the acquisition is successful.